In the UK, employment data released showed that the unemployment rate stayed at 5.1% and the employment rate remained the same at 74.1% - the joint highest since records began in 1971. Average earnings including bonuses have continued to rise beating forecasts of 2% growth, coming in at 2.1%. Wages are still not increasing as fast as members of Bank of England’s Monetary Policy would like.

UK Chancellor George Osborne released his annual budget report. Key points on the budget:

• UK economy is forecast to grow at a slower rate than previously expected, with revised growth of 2.2% in 2016 and 2.4% in 2017 but is expected to be the fastest growing advanced economy.

• Total government debt is expected to have risen over past year to 83.7% of GDP breaking one of Osbornes Fiscal rules

• Another one of his rules to run a surplus by 2020 also appears optimistic with growth downgrade

• Corporate tax to be cut to 17% in 2020

• Personal Allowance raised to £11,500 in 2017

• 40% tax rate raised to £45,000 per year in 2017

• Sugar tax expected to raise £520M

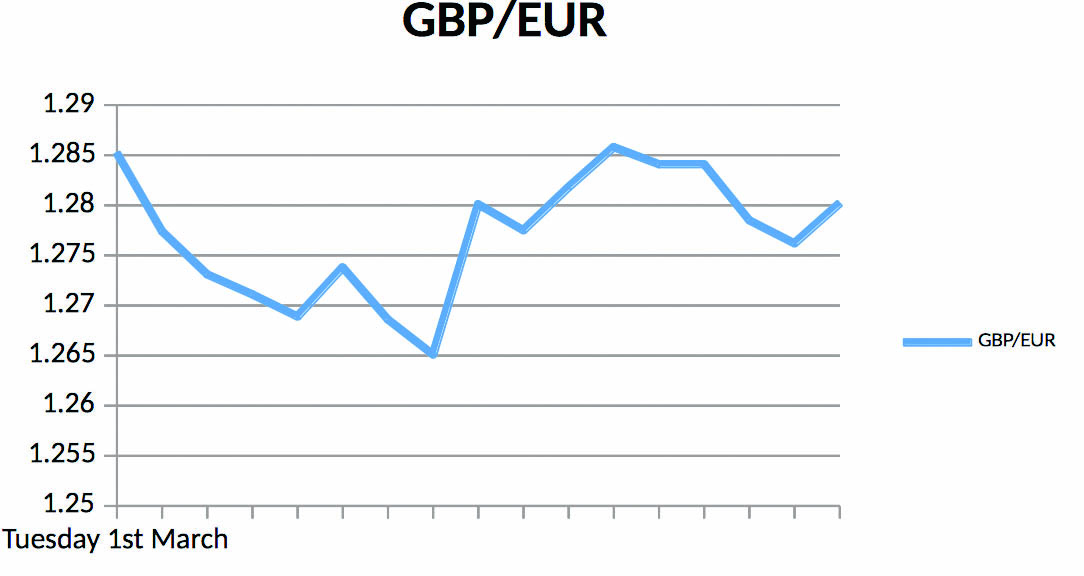

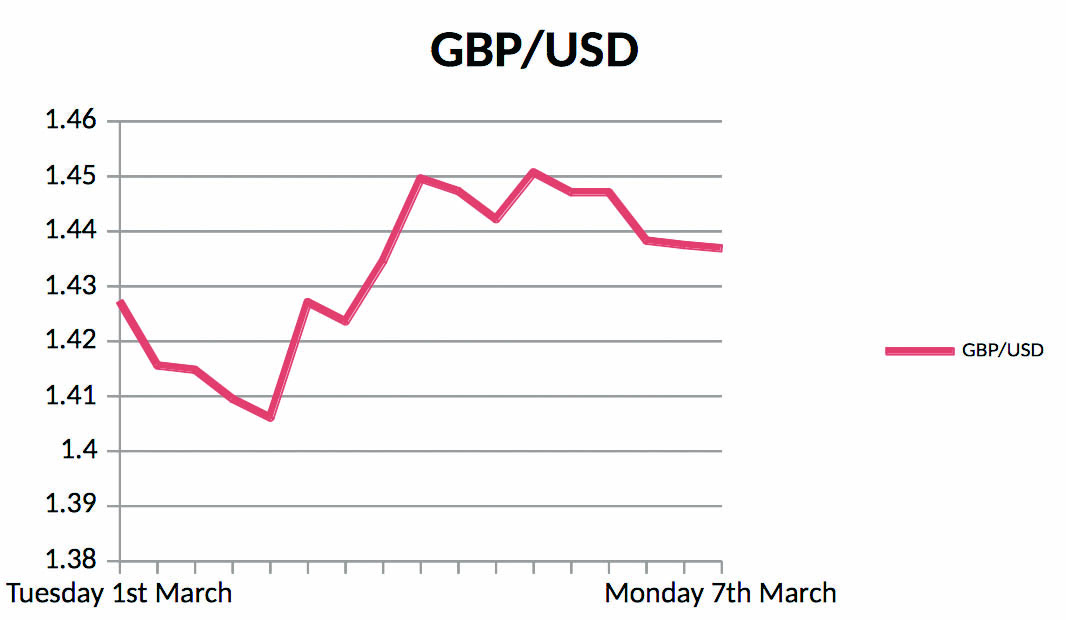

Following the dovish statement from the FOMC on Thursday Sterling continued its upwards rally and was on track for its best daily gain in a year. The MPC kept all monetary policy indicators the same with the official bank rate remaining at 0.5%, asset purchase facility maintained at 375B and the MPC votes remaining the same at 0-0-9. However the resulting conference was used as a forum to notify market participants that the BOE is expected to keep interest rates unchanged as expected and said rates were more likely to rise than not over the next three years.

With the ECB last week cutting interest rates and expanding their monetary policy; the statement from the BOE was interpreted as bullish by market participants who contributed to the gains shown by GBP across the board. Nevertheless, the gains seen by GBP yesterday are still overshadowed by the Brexit with investors worried about the growth forecast should Britain leave the EU.

Figures from the US revealed retail sales dropped in February, but were likely held down by lower prices. The figure, which is not adjusted for inflation, showed spending at retailers fell 0.1 per cent from February to $447.3bn as sales dipped in eight of the 13 retail sub-sectors. Some economists have said that the strong dollar may also be holding down prices, leading to falling sales in a number of sectors. A strong dollar reduces import prices, which can reduce selling prices if passed on to shoppers. Others believe the drop in retail sales are a sign that economic growth has softened. The producer prices (PPI) also fell in February on lower energy and food costs, but prices were unchanged from a year ago, suggesting the downward trend was near to an end. This was the first time since January 2015 that the year-on-year PPI didn’t decline.

The Fed kept its interest rates at 0.5%. The decision is second time in a row now it has decided to keep rates the same since they raised them in December.

The dollar rose against most major currencies, recovering from a five-month low, as traders exited short positions after two straight days of selling in the wake of the Federal Reserve's cautious view on global market developments, announced last Thursday. It was down by just over 1 percent for the week, marking the third straight week of losses for the index.

In a quiet week for data release from the Eurozone; Industrial production in the Eurozone bounced back in January to reach its highest volume of production for industries from factories and manufacturing since 2008. Up trends are regarded as inflationary and generally seen as bullish for the Euro whilst down trends are generally dovish. The month on month reading was anticipated significantly higher than the previous month at to be 1.7% against a previous of -0.5%. The reading was released at 2.1%, 0.4% higher than forecast and thus the euro made some marginal gains against its counterparties. The revised year on year figure consequently rose to 2.8%, coming in significantly better than the previous month’s figure of -0.1%. Euro Area producer price index came out worse than expected on Friday morning, contracting 3.0% versus expectations of only a 2.6% contraction on an annual basis. This provided added reason to buy EUR on the day and contributed to the market's momentum of exiting USD shorts.