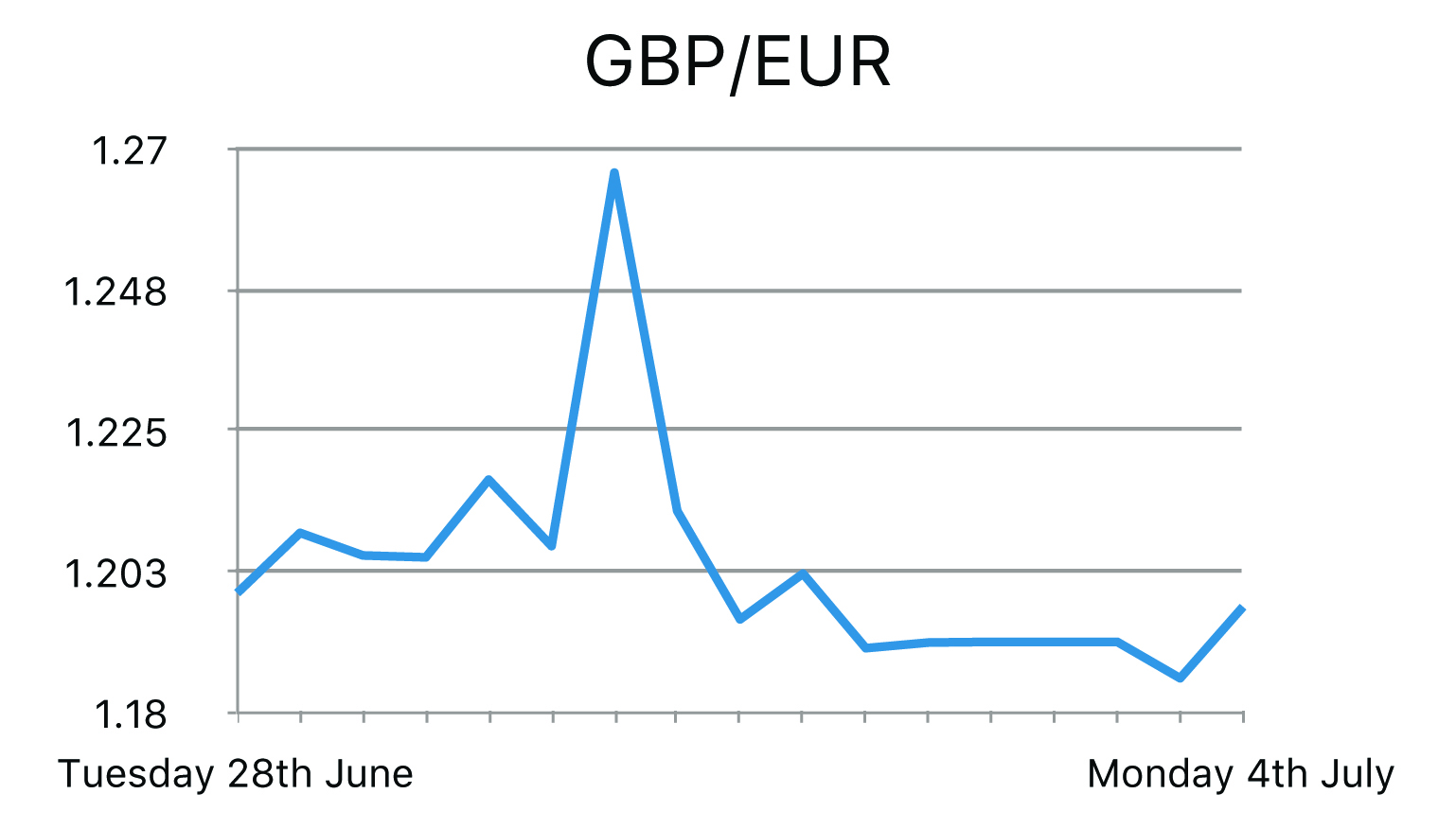

On Tuesday 28th June UK financial markets remain volatile in the wake of the Brexit vote, with sterling plunging to a 31-year low against the dollar after Standard & Poor and Fitch downgraded the UK’s credit rating yesterday. S&P downgraded the UK's rating by two notches, from AAA to AA, with a negative outlook and Fitch also downgraded the UK, from AA+ to AA with a negative outlook. Property shares were badly hit, prompting a trading halt. On Tuesday Day 1 of the EU Economic Summit took place in Brussels. European Union lawmaker’s stated that the UK should exercise article 50 of the Lisbon Treaty as soon as possible. Furthermore, Nigel Farage took the opportunity to speak to its members, saying that he had achieved his ultimate goal and that the referendum’s result was a reaction to Europe’s intention to impose a political union by “stealth” and “deception” and that policy makers are in denial about their failures. In addition, Angela Merkel, in what seems her toughest comment yet, warned the U.K. to have no illusions about life outside the European Union while meeting David Cameroon for his final EU summit following last week’s result. At the same time Jeremy Corbyn loses no confidence vote by 172 to 40 as Labour MPs try to remove him as party leader after his ‘weak’ remain campaign. On Thursday last week no key data was released. However, Bank of England officials met with Britain’s biggest lenders to discuss the impact on the financial system of the country’s vote to leave the EU. Officials calmed fears and assured bosses of the liquidity in the market and also pressed banks to keep lending to investors and businesses in an effort to avoid the repeat of the ‘Credit Crunch’ that hit in 2008. The main headline of Friday was Governor of the Bank of England, Mark Carney saying the BoE could ease monetary stimulus over the summer following the shock result of a Brexit. The seasonally adjusted Markit/CIPS Purchasing Managers’ Index (PMI) posted 52.1, up from a revised reading of 50.4 in May, its highest level since January. Whilst the figure was positive it should be noted that the data collection window for this month’s survey was between the 13th and 27th June. Almost all of the responses included in the final index readings were received prior to the end of 23rd June (the day of the UK’s EU referendum).

In Europe German Chancellor Angela Merkel and fellow European leaders kicked off a series of crisis talks, she urged Britain to get on with it. “An extended waiting game” was bad for both sides, she said. Europe’s leaders must decide how to treat Britain in the divorce talks and what steps to take to reinforce confidence in a bloc set to shrink with the departure of its second-biggest economy. She said, though, it may take some time for the government to invoke Article 50 that triggers the countdown to an EU exit. During the meeting Donald Tusk and Angela Merkel both reiterated the fact that; ‘Access to the single market requires acceptance of all four freedoms’, a reference to EU principles on the free movement of capital, services, goods and Labour. This toughened stance means that the UK cannot have an ‘a la carte access to the single market’ by picking and choosing which parts of the EU it has access to. Furthermore it is widely expected that the ECB will again expand the current monetary policy in a bid to push inflation to their target level of 2%. Although current expansionary monetary policy measures have proven to have been positive for inflation; it is yet to have the desired effect which has also been exacerbated by the vote for Britain to leave the EU last week. The ECB is unlikely to follow the BoE with an immediate response to the prospect of further monetary policy easing, preferring to wait for more tangible evidence that the expected negative impact is materializing.

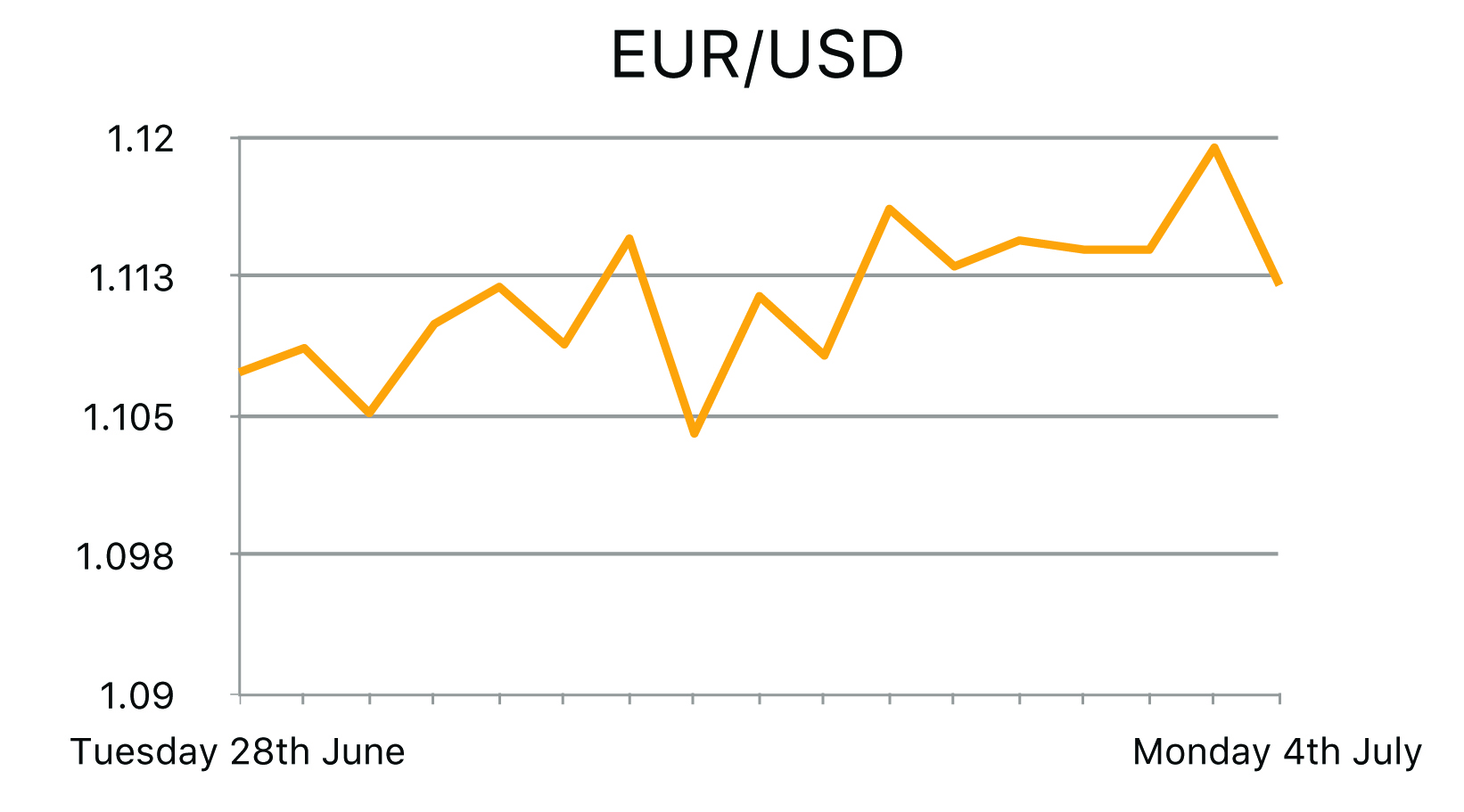

In the US Final gross domestic product quarter on quarter was released at 1.1% on Tuesday, which is slightly better than forecast at 1.0%. However, undermining the dollar, US money markets are pricing out any chance of the Federal Reserve raising interest rates in the coming months, most likely due to potential impact and systemic ramifications of a Brexit on global financial markets - as mentioned by Fed Chair Janet Yellen at the previous FOMC meeting. Also Oil prices jumped more than 2 percent on Wednesday after the U.S. government reported a larger-than-expected weekly drawdown in crude inventories, adding fuel to an existing rally on fading concerns over Britain's exit from the European Union. On Friday the weekly unemployment claims figure from the US was printed marginally better than forecast at 286k against a forecast of 287k. Although the figure is commonly associated as a key indicator to economic health, many investors are more concerned or focused on the forward guidance surrounding a potential rate hike, if any. Given the recent Brexit vote, the Fed will be keeping a close eye on the systemic ramifications on global financial markets and how this impacts the US economy and job market. The indexes for both new orders and production rose in June, and both have been expanding for the past six months.