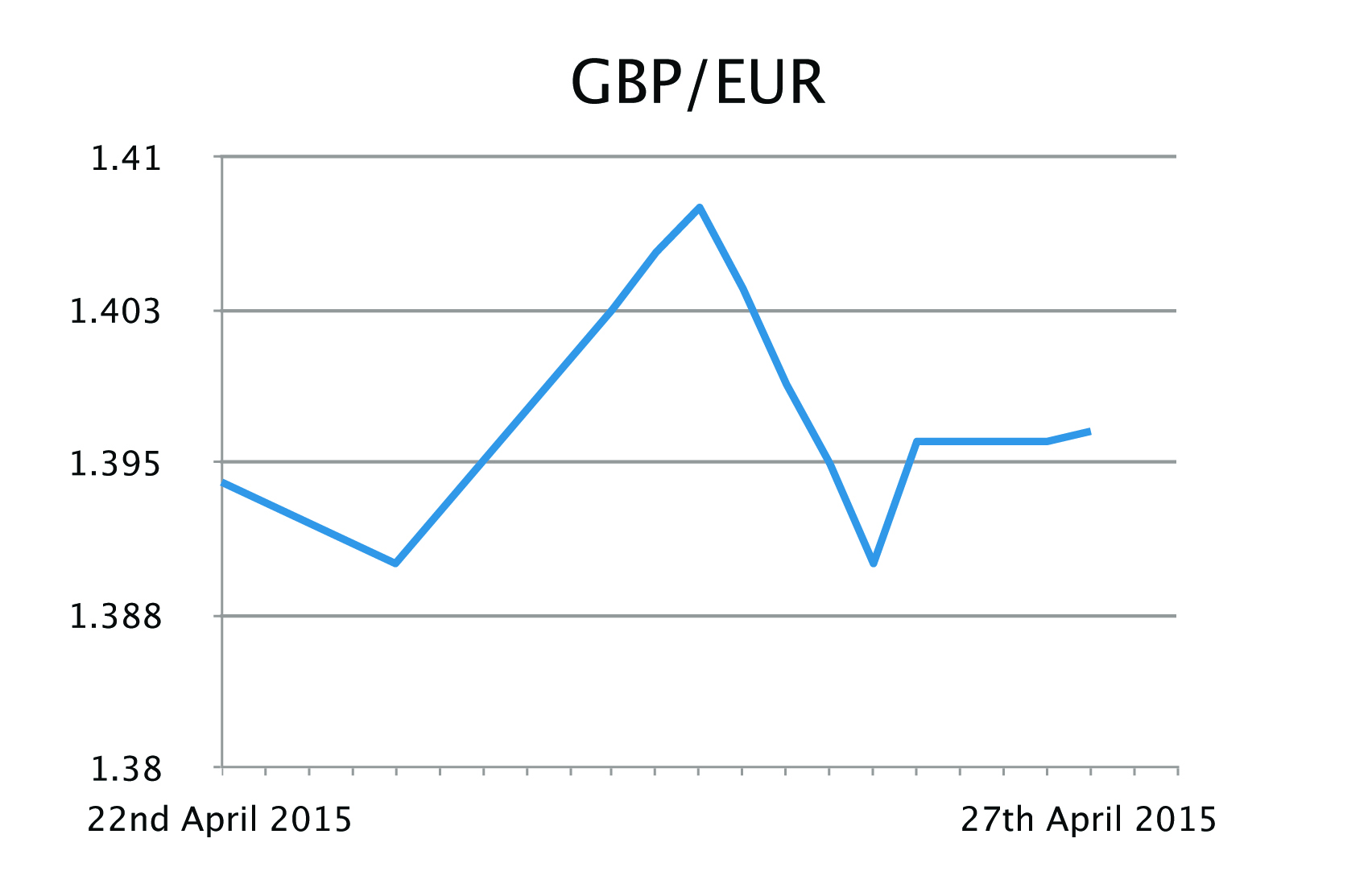

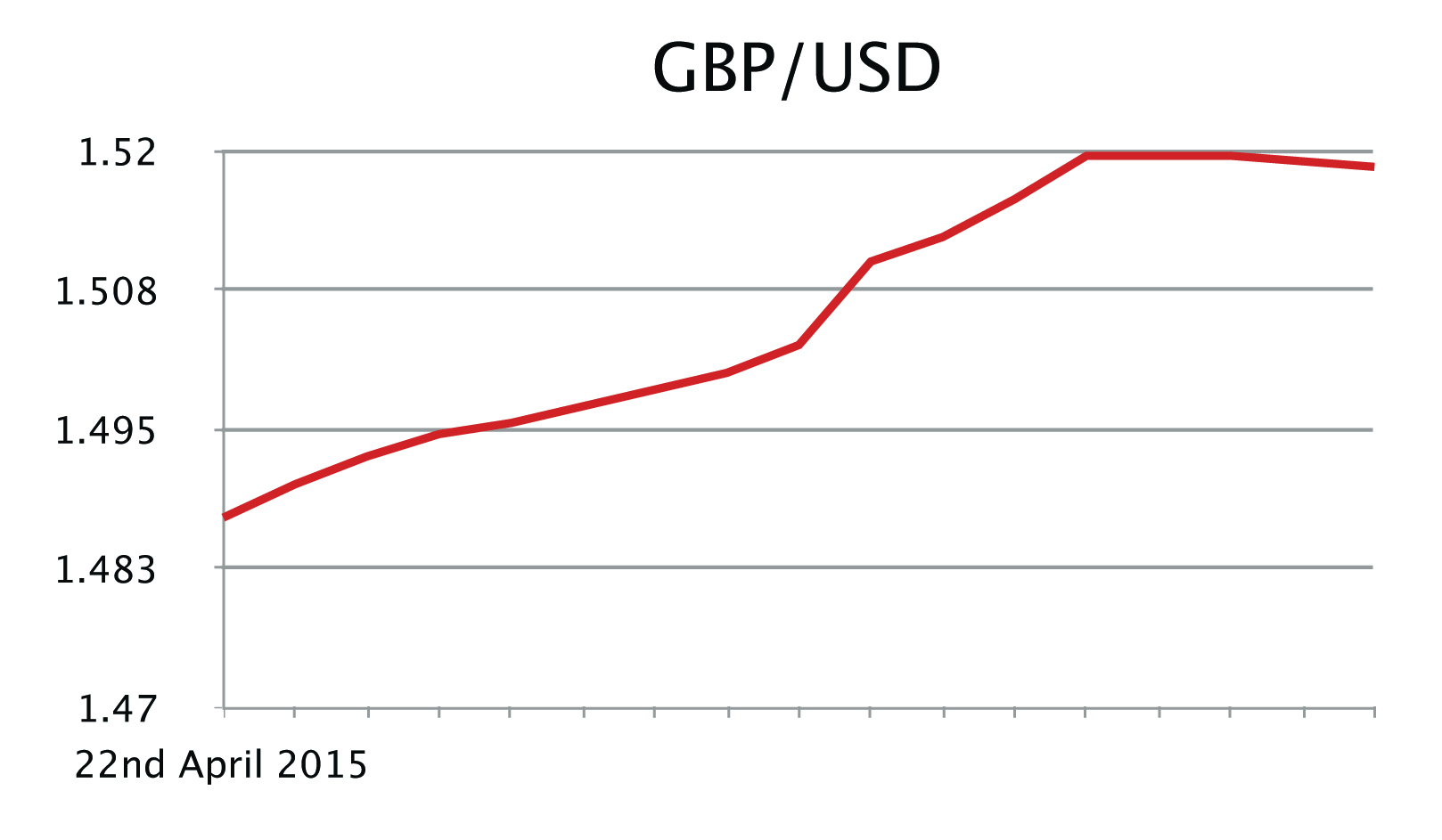

The monetary policy committee announced a unanimous decision to keep interest rates unchanged at 0.5%. The key announcement was all of the members deciding that the next interest rate adjustment would be to the upside, eliminating concerns over interest rate cuts due to low inflation. These comments caused a sharp rally of the Pound, gaining over 1% against both the Euro and the Dollar. Elsewhere in the news, the latest election polls showed the Conservatives leading at 35% with Labour marginally behind at 34%.

The Pound had a mixed session after disappointing retail sales figures were offset by a positive government borrowing figure, providing a varied set of data as parties spar over the economy in the run-up to the general election. The poor retail sales figure is believed to be a backlash of consumers being maxed out after taking advantage of the discount-fuelled frenzies we saw over the festive period. Despite the disappointing retail figures, the Pound was boosted by separate figures showing the budget deficit narrowed more than officials estimated after Britain posted the smallest shortfall for 11 years.

Government borrowing fell to £7.4bn in March, taking the total for the financial year to £87.3bn, well below the £90.2bn figure estimated by the independent Office for Budget Responsibility and £11.1bn lower than last year's total. The timely figure was perceived by analysts as demonstrating the good the current government has done for the economy.

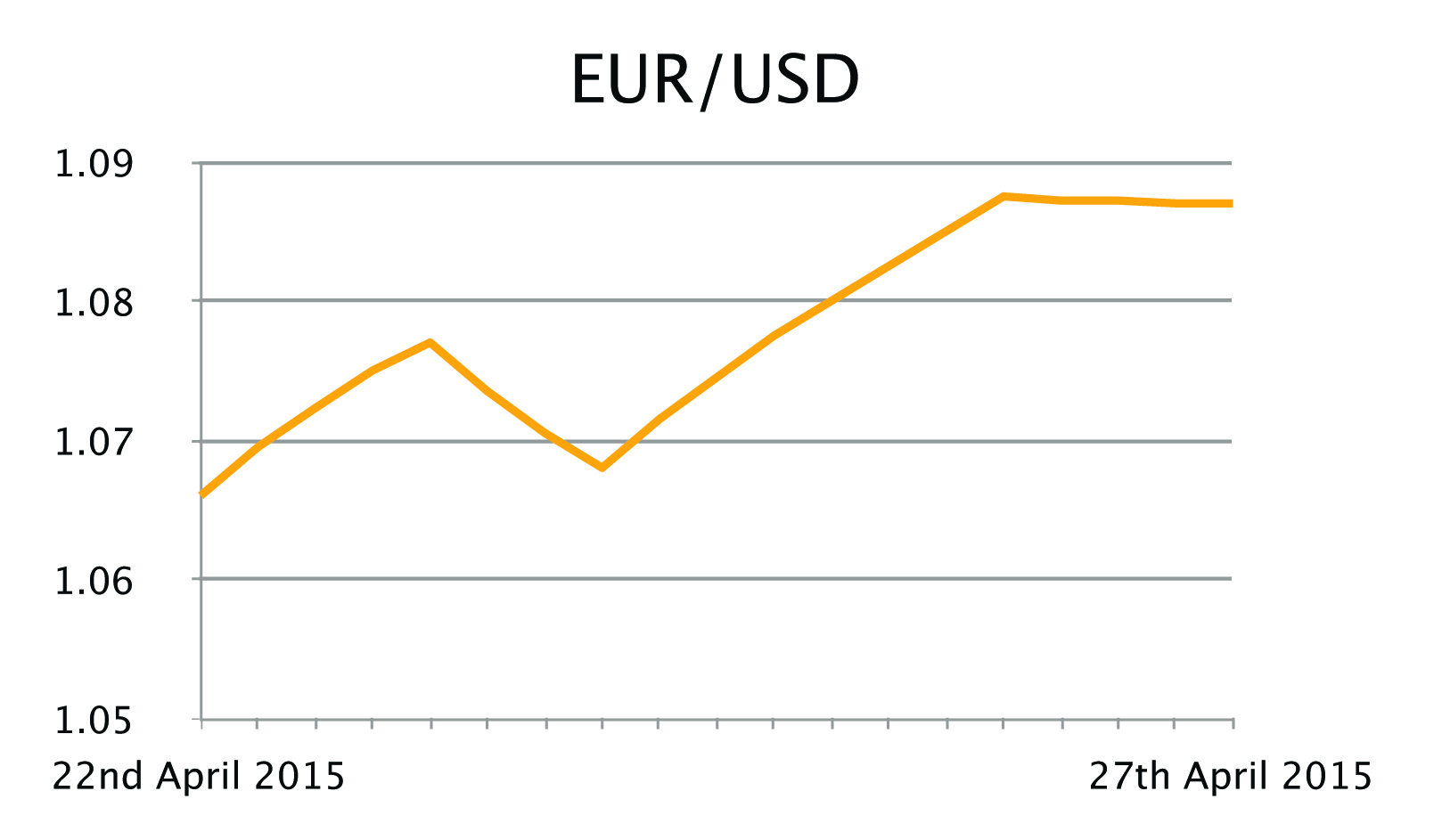

There was market talk last week Thursday 23rd April that despite continued setbacks in negotiations between Greece and their European counterparts, some progress is being made. Creditors have reduced demands for Greece and say there could be scope for a potential short term Greek default in order to allow more time for negotiations.

The Euro fought back after French and German manufacturing came in significantly below forecast first thing. Both figures signalled an easing in the rate of expansion of private sector output to near stagnation in April. Analysts believe this weaker Euro-zone expansion is a sign that bond purchases by the European Central Bank will take time to revive a fragile recovery. While ECB President Mario Draghi has already pointed to some positive effects created by the 1.1 trillion euro plan, he has also cautioned that the region’s recovery won’t be sustainable without government reforms. Investors have begun to lose some of their confidence in the performance of Germany, Europe’s largest economy, as global weakness damped export prospects.

The Dollar weakened after unemployment claims came out above forecast, despite holding below 300,000 for the seventh straight week, pointing to a rebound in payrolls after hiring eased last month. Muted firings are helping boost prospects of a healthy labour market even as employers slowed hiring in March amid weaker foreign demand, chillier temperatures and fallout from the West Coast port workers’ dispute. Projections for more robust employment growth ahead may keep Federal Reserve officials on course to raise the benchmark interest rate this year for the first time since 2006.