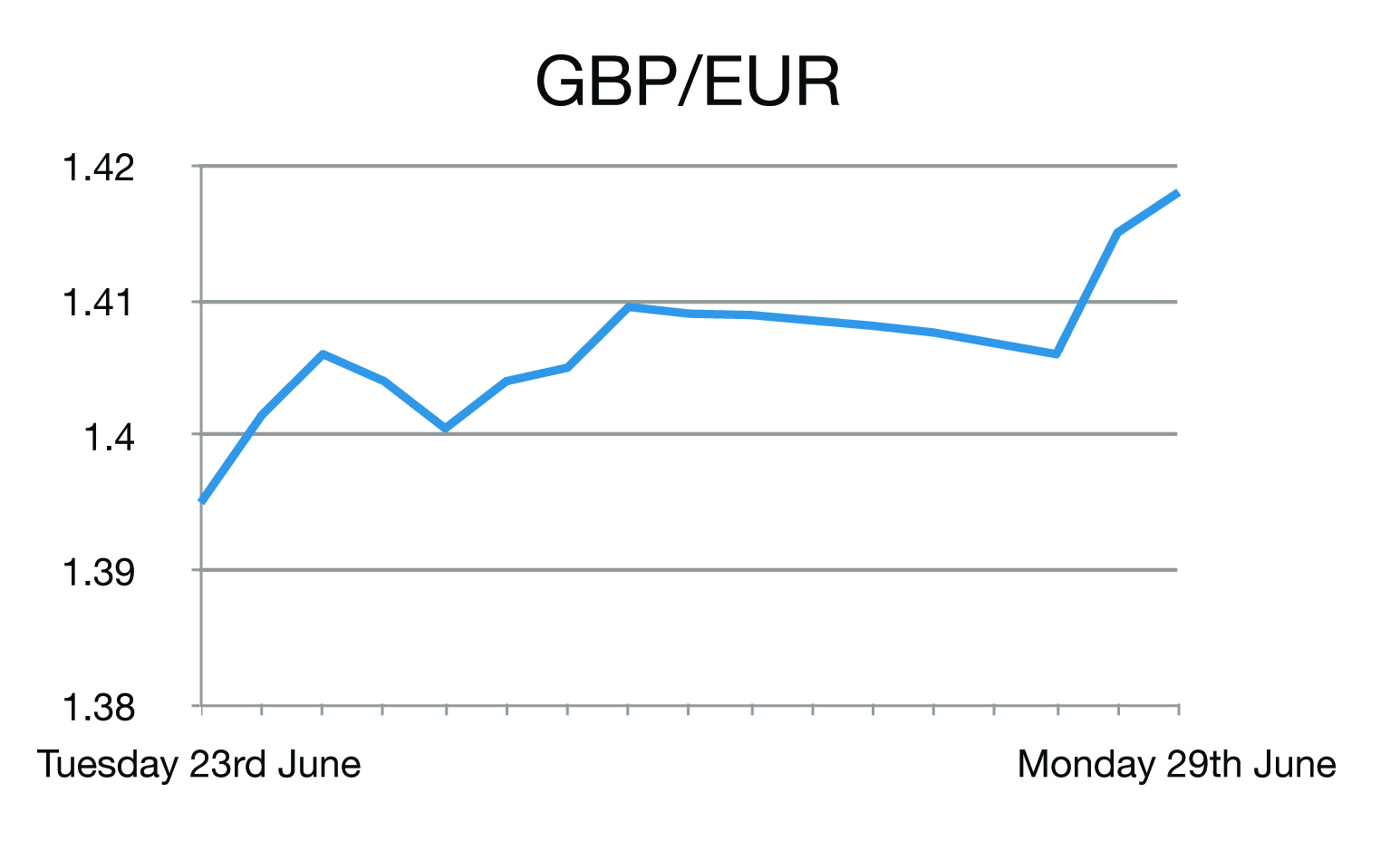

Over the weekend Greek banks and the stock exchange will be shut for at least a week after creditors refused to extend the country's bailout and savers queued to withdraw cash, taking Athens' stand-off with the European Union and the International Monetary Fund to a dangerous new level. Greece's banks have been kept afloat by emergency funding from the European Central Bank and are on the front line as Athens moves towards defaulting on a 1.6 billion euros payment due to the International Monetary Fund on Tuesday.

Greece's left-wing Syriza government had for months been negotiating a deal to release funding in time for its IMF payment. Then suddenly, in the early hours of Saturday, Tspiras asked for extra time to enable Greeks to vote in a referendum on the terms of the deal. Creditors turned down this request, leaving little option for Greece but to default, piling further pressure on the country's banking system.

Creditors want Greece to cut pensions and raise taxes in ways that Tsipras has long argued would deepen one of the worst economic crises of modern times in a country where a quarter of the workforce is already unemployed. Many leading economists have voiced sympathy with the Greek government's argument that further cuts in spending risk choking off the growth which would give Greece some prospect of servicing debts worth nearly twice its annual national income.

International Monetary Fund boss Christine Lagarde said that if the July 5 vote produced "a resounding yes" to remain in the euro and fix the Greek economy then the creditors would be willing to make an effort.

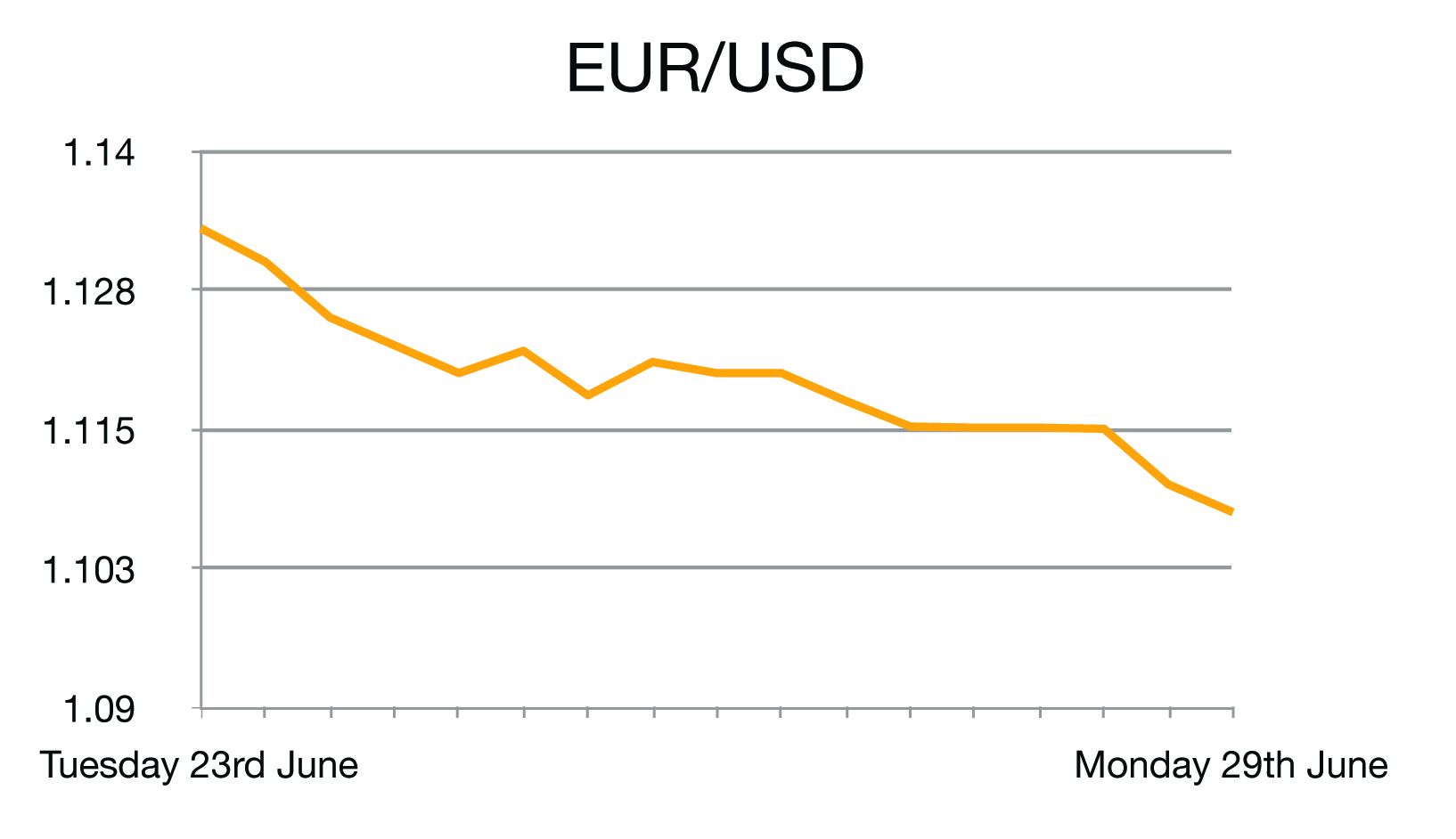

In other European news last week German business morale weakened for a second straight month in June, suggesting concerns about the Greek debt crisis are hitting the mood amongst companies across Europe's largest economy. IFO's business climate index dropped to 107.4 in June from 108.5 in May. That was its weakest reading since February this year.

Also the index for the Euro area factory and services unexpectedly rose to the highest in more than four years this month as growth gained momentum in Germany and France. France’s gauge of the two industries climbed to the highest since 2011 and growth in Germany also strengthened. European Central Bank stimulus and a weaker euro helped boost euro-area growth to 0.4 percent in the first quarter.

In the US Orders for business equipment rose in May for just the second time this year, indicating demand for American-made manufactured goods is stabilizing. Orders for non-military capital goods excluding aircraft rose 0.4 percent last month after a 0.3 percent decline in April, orders for all durable goods declined 1.8 percent.

Exports will probably take longer to rebound as the dollar’s appreciation makes American-made goods less competitive globally. A pick-up in business investment would go a long way towards boosting growth in the world’s largest economy, which suffered a setback in the first quarter amid harsh winter weather, a strong dollar and delays at ports.

It was also reported the world’s largest economy shrank less in the first quarter than previously estimated, aided by a bigger gain in consumer spending. GDP in the U.S. only fell at a 0.2 percent annualized rate, revised from a previously reported 0.7 percent drop. The harsh winter weather and port delays that damped growth at the start of the year have given way to increases in consumer spending and housing, boosting Federal Reserve projections that the setback was temporary.

Still hindering growth in the US are lower oil prices which is hitting investment in the energy industry. Also a strong dollar continues to hurt exporters.

It was a quiet week for the UK however property sales data has provided more evidence that the UK housing market is moving more slowly than a year ago. A total of 98,540 homes were sold in May, down 35 from the same time last year